For many landlords in 2026, the question is no longer just about which property to buy, but how to own it. At Mortgage Bazaar, we’ve seen a record-breaking surge in incorporation, with over 66,000 new Buy-to-Let companies established in the UK last year alone.

Deciding between personal ownership or a limited company (often called a Special Purpose Vehicle or SPV) is a high-stakes choice that affects your tax bill, mortgage rates, and future growth.

1. The “Section 24” Factor: Why the Shift?

The primary driver behind the move to limited companies is Section 24. For individual landlords, mortgage interest is no longer a deductible expense; instead, you receive a flat 20% tax credit.

- Personal Ownership: If you are a higher-rate (40%) or additional-rate (45%) taxpayer, you are effectively taxed on your gross rental income before interest is paid, which can lead to tax bills that sometimes exceed your actual cash profit.

- Limited Company: Companies are exempt from Section 24. You can deduct 100% of your mortgage interest and other running costs before paying Corporation Tax (currently 19–25% depending on profit levels).

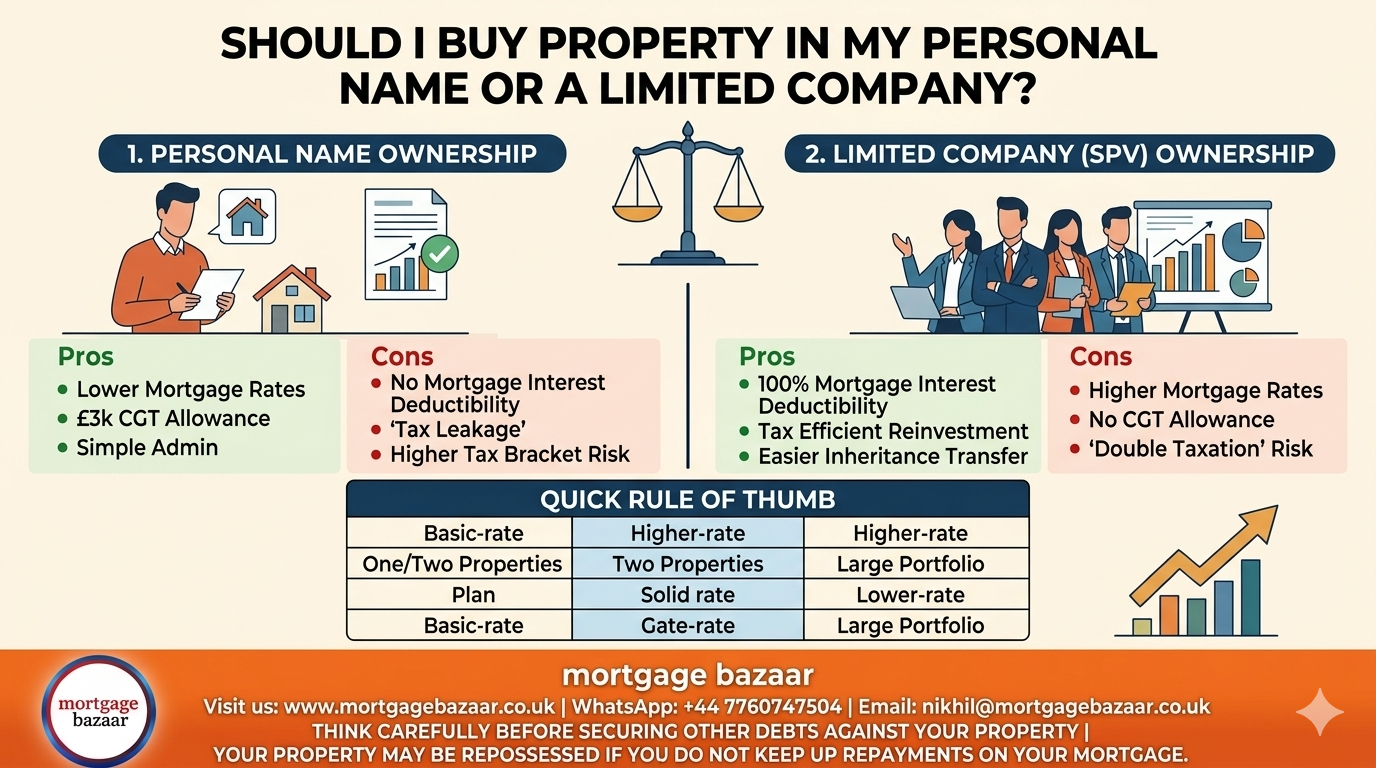

2. Buying in Your Personal Name

Despite the tax shifts, personal ownership remains a viable—and often simpler—option for many.

The Pros:

- Lower Mortgage Rates: Standard Buy-to-Let mortgages are generally 0.3% to 0.75% cheaper than limited company products.

- Capital Gains Tax (CGT) Allowance: Individuals benefit from an annual CGT allowance (£3,000 for 2025/26). Gains are taxed at 18% (basic rate) or 24% (higher rate).

- Simplicity: You avoid the administrative burden of filing annual company accounts and the costs of a specialist property accountant (typically £1,000+ per year).

The Cons:

- Tax Inefficiency: Higher-rate taxpayers face significant “tax leakage” due to the inability to fully offset finance costs.

- Increased Taxable Income: Rental income is added to your other earnings, which could push you into a higher tax bracket or affect your entitlement to Child Benefit.

3. Buying via a Limited Company (SPV)

If your goal is to build a professional portfolio, the limited company structure is often the gold standard.

The Pros:

- Full Interest Deductibility: Your mortgage interest is treated as a business expense, significantly lowering your taxable profit.

- Reinvestment Power: By keeping profits within the company, you only pay Corporation Tax, leaving more capital available to fund your next deposit.

- Inheritance Tax Planning: It is often easier to transfer company shares to family members than to transfer physical property deeds.

The Cons:

- Higher Costs: Expect higher interest rates and arrangement fees from lenders.

- “Double Taxation”: You pay Corporation Tax on profits, and then personal Income Tax (dividend tax) if you want to withdraw those profits for personal use.

- No CGT Allowance: Companies do not receive a tax-free allowance when selling property; instead, the entire gain is subject to Corporation Tax.

4. Which Route is Right for You?

At Mortgage Bazaar, we recommend using this quick rule of thumb to start your decision-making process:

| Scenarios where Personal Name wins: | Scenarios where Limited Company wins: |

| You are a basic-rate taxpayer. | You are a higher or additional-rate taxpayer. |

| You only plan to own one or two properties. | You plan to build a larger portfolio. |

| You need the rental income for daily living costs. | You intend to reinvest profits to grow your business. |

| You plan to sell in the short-to-medium term. | You are looking for long-term multi-generational wealth. |

5. How Mortgage Bazaar Can Assist

The 2026 mortgage market is complex, but you don’t have to navigate it alone. Whether you choose the personal or company route, we provide:

- Specialist SPV Access: We work with lenders who specifically support limited company structures, including HMOs and multi-unit blocks.

- Personalized Comparison: We can help you model the true cost of a personal vs. company mortgage, including all fees and interest rates.

- Fast-Track Applications: Our 14-day average processing time applies to both personal and limited company applications.

Ready to make your choice?

Before you commit, it is vital to speak with a tax advisor to confirm your specific tax position. Once you have your strategy, Mortgage Bazaar will find the perfect product to match it.

- WhatsApp us: +44 7760747504

- Email: nikhil@mortgagebazaar.co.uk

- Visit us: www.mortgagebazaar.co.uk

Disclaimer: THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST YOUR PROPERTY | YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Visit us: - https://g.page/r/CfbGE7O83tmREAE

- https://www.facebook.com/mortgagebazaaruk

- https://www.instagram.com/mortgagebazaaruk

- https://www.linkedin.com/company/mortgagebazaar

Leave a Reply