The UK property market of 2026 is a different beast than the one we navigated just a few years ago. The era of frantic bidding wars and “offers over” madness has largely stabilized into what experts call a classic Buyer’s Market. With property inventory at a 12-year high and the Bank of England base rate holding steady at 3.75% as on 30th April 2026, the power has shifted.

At Mortgage Bazaar, we are seeing a unique phenomenon: savvy buyers are realizing that a “low deposit” is no longer a barrier to a “high potential” home. In a market where you have the luxury of time and choice, your 5% or 10% deposit is a powerful tool—if you know how to use it.

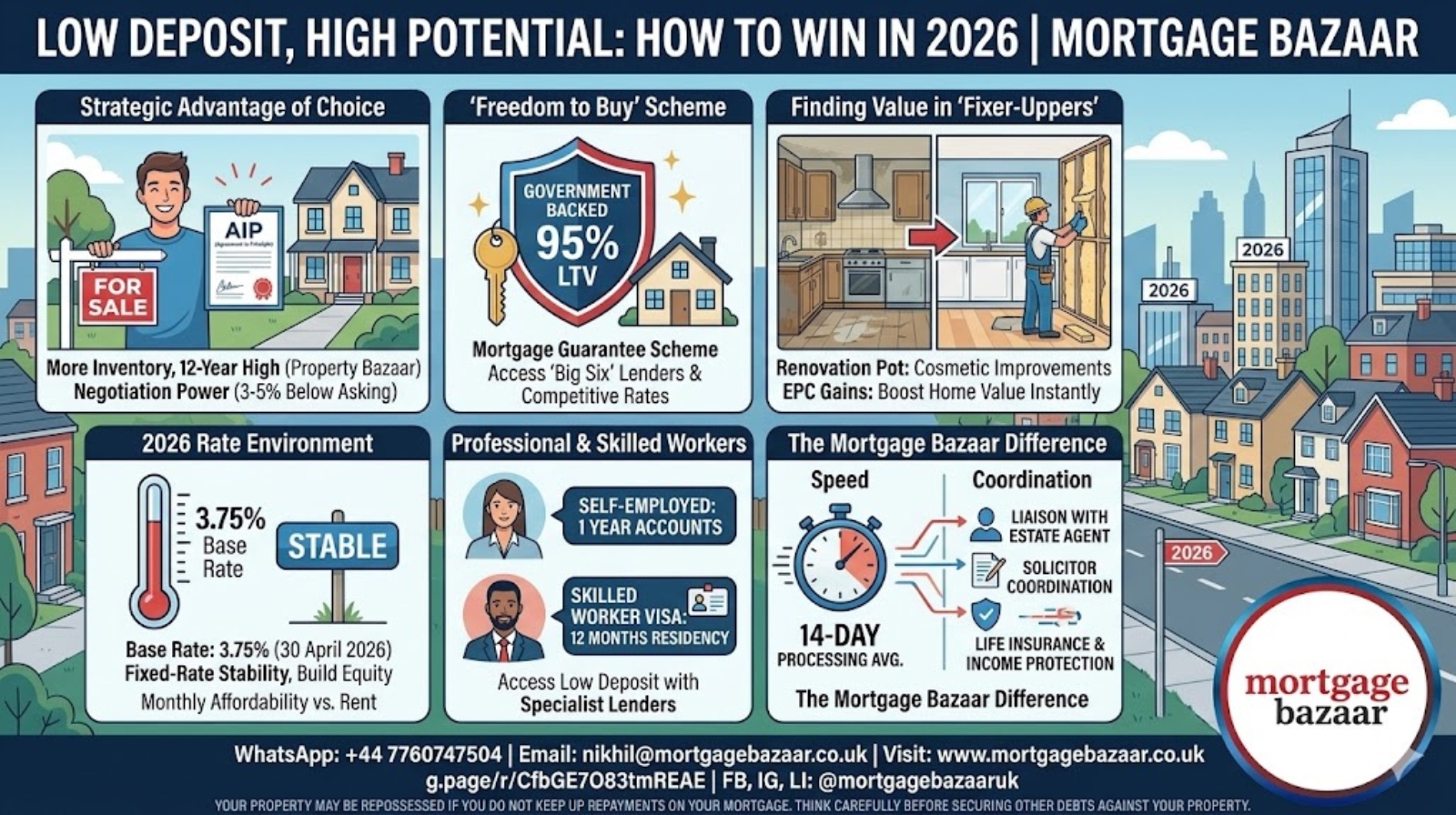

Here is how you can win big in the 2026 market using a low-deposit strategy.

1. The Strategic Advantage of Choice

In a “Seller’s Market,” buyers with 5% deposits are often overlooked in favor of cash buyers or those with 40% equity. In 2026, the script has flipped. Because there are more homes for sale than there are active buyers, sellers are much more inclined to work with you, regardless of your deposit size.

- Negotiation Power: In 2026, it is common for properties to sell for 3% to 5% below the asking price.

- The “Agreement in Principle” (AIP) Edge: Even with a 5% deposit, having an AIP from Mortgage Bazaar proves to the seller that you are a “ready-to-go” buyer. In a crowded market of properties, a verified buyer is a seller’s best friend.

2. Leveraging the “Freedom to Buy” Scheme

The year 2026 marks the first full year of the government’s permanent Mortgage Guarantee Scheme, often referred to as “Freedom to Buy”. This scheme is the backbone of the low-deposit market.

- How it Works: The government provides a guarantee to lenders, encouraging them to offer 95% Loan-to-Value (LTV) mortgages.

- Why it Matters: This has brought the “Big Six” lenders back into the low-deposit space with competitive rates. You no longer have to pay a massive premium just because your deposit is small. At Mortgage Bazaar, we compare these government-backed products across 200+ lenders to ensure you get the best deal.

3. High Potential: Finding Value in the “Fixer-Upper”

In a buyer’s market, you can afford to look for properties with “added value” potential. With a low deposit, your goal is to grow your equity as fast as possible.

- Cosmetic Renovations: Look for homes that need a new kitchen, flooring, or a fresh coat of paint. Because you saved on the deposit, you might have a small “renovation pot” of cash left over.

- Energy Efficiency (EPC) Gains: In 2026, energy efficiency is a huge price driver. Buying a home with a lower EPC rating at a discount and upgrading the insulation or windows can instantly increase the property’s market value, effectively “earning” you a higher deposit for when you next remortgage.

4. Understanding the 2026 Rate Environment

While the 3.75% base rate is higher than the historical lows of 2021, it is significantly lower than the peaks of 2023.

- Monthly Affordability: Many buyers find that the monthly cost of a 95% mortgage is now comparable to—or even cheaper than—local rental prices, which have seen sharp increases in early 2026.

- Fixed-Rate Stability: Locking in a 5-year fix now provides the stability needed to ignore market fluctuations while you build up your “homeowner’s equity.”

5. The Professional & Skilled Worker Advantage

At Mortgage Bazaar, we specialize in “non-standard” success stories. 2026 is a fantastic year for:

- Self-Employed Professionals: With just 1 year of accounts, we can help you secure a 5% or 10% deposit mortgage.

- Skilled Worker Visa Holders: International professionals can now access low-deposit mortgages with as little as 12 months of UK residency.

In a buyer’s market, these specialist lenders are even more eager to support high-income professionals who are contributing to the UK economy.

6. Closing the Deal: The Mortgage Bazaar Difference

The 2026 market moves at a steady pace, but when a “high potential” home appears, you still need to act with precision.

Our 14-day average processing time means that while other buyers are waiting for their banks to call them back, your offer is already moving toward completion. We don’t just find you a loan; we manage the entire ecosystem of your purchase:

- Direct Liaison: We talk to your estate agent to strengthen your offer.

- Solicitor Coordination: We keep the legal chain moving to prevent “gazumping” or chain collapses.

- Comprehensive Protection: We ensure your new home is protected with Life Insurance and Income Protection, so your low-deposit investment is never at risk.

Final Thoughts: Fortune Favors the Prepared

The 2026 “Buyer’s Market” is a window of opportunity that won’t stay open forever. By utilizing a low-deposit mortgage, you can secure a property at a fair price and begin your journey of wealth creation through homeownership.

Stop waiting for a 20% deposit while house prices continue to stabilize and grow. Your 5% is enough to win in today’s market.

Start Your Journey Today

Ready to see how much you can borrow? Contact the expert team at Mortgage Bazaar for a free, no-obligation consultation.

- WhatsApp us: +44 7760747504

- Email: nikhil@mortgagebazaar.co.uk

- Visit us: www.mortgagebazaar.co.uk

Disclaimer: THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST YOUR PROPERTY | YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Visit us: - https://g.page/r/CfbGE7O83tmREAE

- https://www.facebook.com/mortgagebazaaruk

- https://www.instagram.com/mortgagebazaaruk

- https://www.linkedin.com/company/mortgagebazaar

Leave a Reply