For years, the biggest barrier to homeownership in the UK hasn’t been the monthly mortgage payments—it’s been the daunting mountain of a deposit. Traditionally, even a “low” 5% deposit on an average £300,000 home required a staggering £15,000 in savings. For many first-time buyers, that figure felt like a finish line that kept moving further away.

But the landscape has changed. At Mortgage Bazaar, we are proud to guide our clients through a new era of accessibility. It is now possible to secure your first home with just a £5,000 deposit, effectively allowing you to borrow up to 98.34% of the property value.

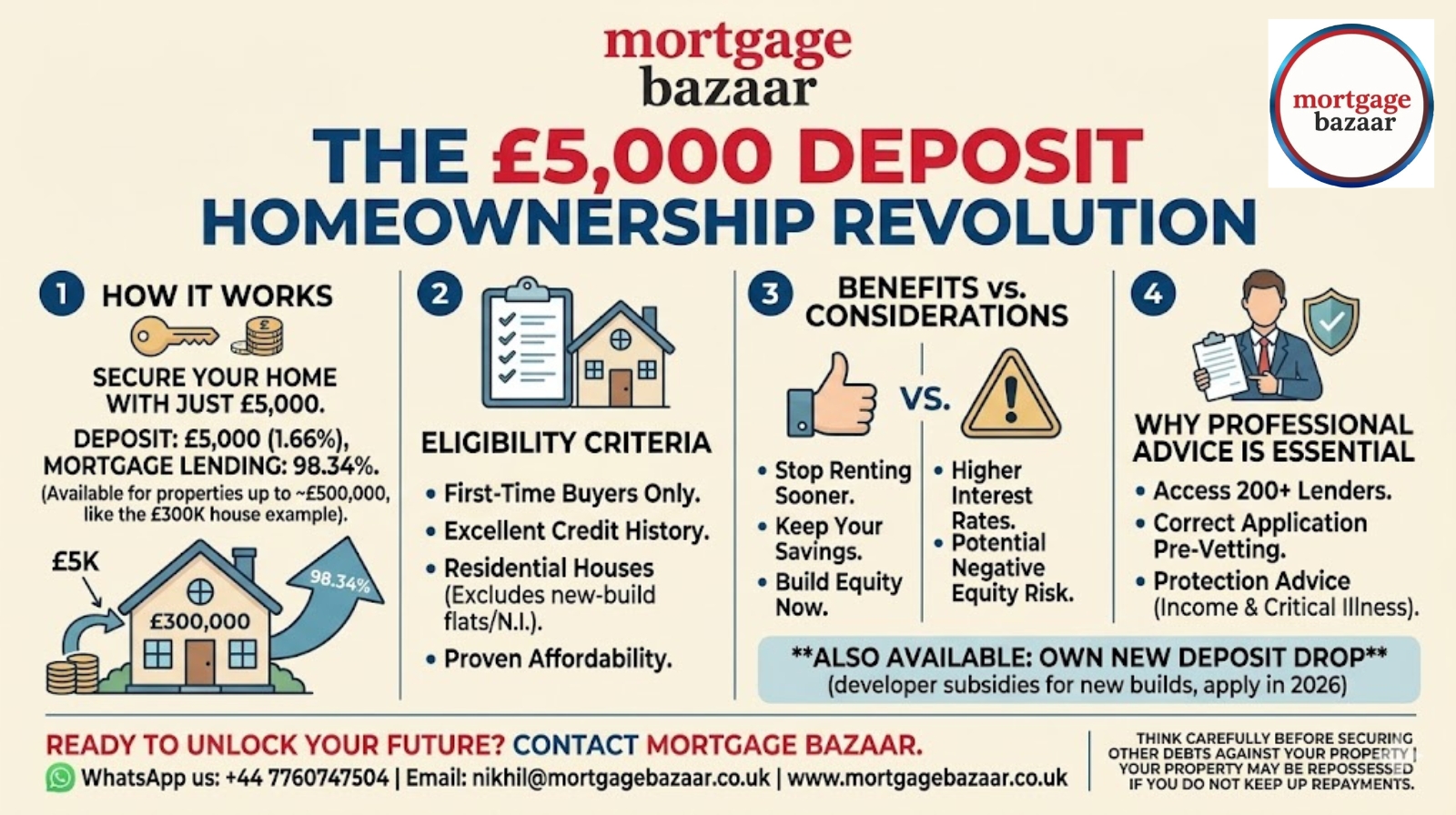

Here is how this revolutionary shift in UK lending works and how you can take advantage of it in 2026.

1. What is the £5,000 Deposit Scheme?

This isn’t a government grant or a “too good to be true” marketing gimmick. It is a specialized mortgage product launched by innovative lenders (such as Yorkshire Building Society and others in the specialist space) to address the “generation rent” crisis.

How the Math Works

Standard mortgages usually stop at 95% Loan-to-Value (LTV). However, these new products are designed for properties up to a certain value (typically £500,000).

- The Traditional Way: On a £300,000 house, a 5% deposit is £15,000.

- The £5K Way: On that same £300,000 house, you pay just £5,000. The lender provides a mortgage for the remaining £295,000.

- The Result: You are borrowing estimated 98.34% of the property’s value.

2. Who is Eligible for a 98.34% Mortgage?

Because the lender is taking on a higher level of risk by lending nearly the full value of the property, the eligibility criteria are specific. At Mortgage Bazaar, we help you ensure you meet these key requirements:

- First-Time Buyers Only: This scheme is strictly reserved for those who have never owned a property anywhere in the world.

- Property Type: The £5,000 deposit scheme is generally for standard residential houses. It usually excludes new-build flats or North Ireland properties, though criteria are constantly evolving.

- Excellent Credit History: Since your equity (deposit) is low, your credit score must be high. Lenders want to see a flawless track record of utility payments, credit card management, and no recent “hard” credit searches.

- Affordability: You must have a stable income that comfortably covers the monthly repayments. Lenders will perform a deep dive into your “disposable income” to ensure you aren’t overstretched.

3. The “Own New” Deposit Drop: Another Way to Buy

While the £5,000 fixed deposit is popular for existing homes, if you have your heart set on a brand-new home, the Own New Deposit Drop is the 2026 game-changer.

This scheme allows you to buy a new-build property with a 5% deposit, but with a twist: the developer contributes to the lender to “subsidize” your interest rate. While it technically requires a 5% deposit, at Mortgage Bazaar, we often combine this with other incentives to reduce your upfront cash burden and drastically lower your monthly payments for the first 2-5 years.

4. Pros and Cons of a High LTV Mortgage

Before jumping in, it is vital to understand the balance of a 98.34% mortgage.

The Advantages:

- Stop Renting Sooner: You could save years of time that would otherwise be spent “chasing the market” to save a larger deposit.

- Keep Your Savings: Instead of emptying your bank account for a 10% deposit, you can keep your “rainy day” fund for furniture, moving costs, and home improvements.

- Build Equity Now: Every month you pay your mortgage, you are paying off your debt, not your landlord’s.

The Considerations:

- Higher Interest Rates: Generally, the more you borrow, the higher the interest rate. 98% mortgages will have higher rates than 90% or 75% LTV products.

- Negative Equity Risk: If house prices were to drop significantly in the short term, you could owe more than the house is worth. However, for those planning to stay in their home for 5+ years, this risk is usually mitigated by long-term market growth.

5. Why Professional Advice is Essential

Applying for a niche product like a £5,000 deposit mortgage is not the same as a standard application. If you apply to the wrong lender and get rejected, the “hard search” on your credit file could make it impossible to apply elsewhere for months.

How Mortgage Bazaar helps:

- Pre-Vetting: We review your credit file and bank statements before talking to lenders to ensure you fit the criteria.

- Access to 200+ Lenders: We know exactly which building societies and specialist banks are currently offering 98% LTV products.

- Holistic Planning: We calculate the total cost over the fixed term to ensure the higher interest rate actually makes financial sense for you.

- Speed: Our average processing time of 14 days ensures you can secure your offer before the lender pulls the product from the market (as these high-demand deals often have limited funding “tranches”).

6. Protection: Keeping Your New Home Safe

When you borrow 98.34% of a property’s value, you have very little “buffer.” If you were to lose your income due to illness or injury, you could quickly fall into arrears.

As part of our home purchasing assistance, we provide tailored advice on Income Protection and Critical Illness Cover. We make sure that if the unexpected happens, your mortgage is covered, and your home remains yours.

Conclusion: 2026 is the Year of Opportunity

The dream of homeownership is no longer reserved for those with tens of thousands in the bank. Whether you are using the £5,000 deposit scheme or the Own New Deposit Drop, the barriers are falling.

Ready to see if you qualify? Don’t spend another year paying someone else’s mortgage. Contact the expert team at Mortgage Bazaar today for a free, no-obligation assessment. We’ll help you find the keys to your first home with just a fraction of the traditional deposit.

- WhatsApp us: +44 7760747504

- Email: nikhil@mortgagebazaar.co.uk

- Visit us: www.mortgagebazaar.co.uk

Disclaimer: THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST YOUR PROPERTY | YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Visit us: - https://g.page/r/CfbGE7O83tmREAE

- https://www.facebook.com/mortgagebazaaruk

- https://www.instagram.com/mortgagebazaaruk

- https://www.linkedin.com/company/mortgagebazaar

Leave a Reply