For years, the UK housing market has felt like a “Catch-22.” You want to buy a home, but high rents make it nearly impossible to save a 20% deposit. You have the income to cover a mortgage, but you’re worried about locking in a 95% Loan-to-Value (LTV) deal when interest rates aren’t at their historic lows.

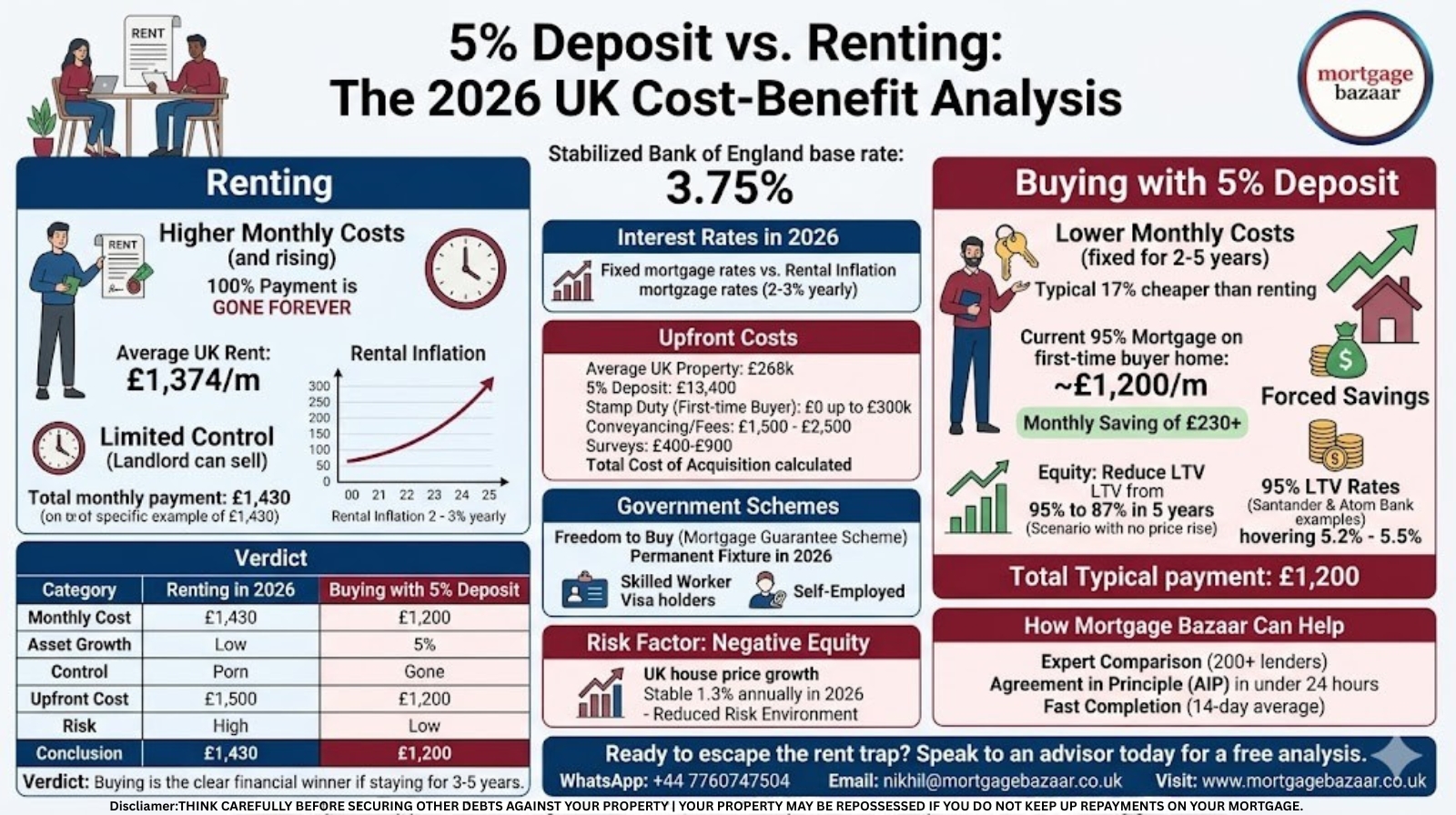

As we move through April 2026, the narrative is shifting. With the Bank of England base rate currently stabilized at 3.75% and rental inflation hitting an average of £1,374 per month across the UK, the “rent vs. buy” debate has reached a tipping point.

At Mortgage Bazaar, we’ve crunched the numbers. Here is the definitive 2026 cost-benefit analysis of buying with a 5% deposit versus staying in the rental market.

1. The Monthly Payment Gap: Rent vs. 95% Mortgage

In many UK cities—including Glasgow, Newcastle, and Nottingham—owning a home with a 5% deposit is now officially cheaper than renting an equivalent property.

According to recent data, first-time buyer mortgage payments are typically 17% cheaper than renting. For example, if you are paying £1,430 (the current average rent in England), a 95% mortgage on a typical first-time buyer home might cost you closer to £1,200. That is a monthly saving of £230—money that goes back into your pocket rather than your landlord’s.

2. The Power of “Forced Savings” (Equity)

When you rent, 100% of your payment is gone forever. When you have a 5% deposit mortgage, a portion of every payment goes toward paying down the principal of your loan. This is what we call “forced savings.”

- Scenario: After five years of owning a home with a 5% deposit, you could reduce your LTV from 95% to 87%—even if property prices don’t rise at all.

- The Result: By 2031, you won’t just have a home; you’ll have a significant stake in an asset that can be used to secure much lower interest rates when you remortgage.

3. Comparing Interest Rates in 2026

Many buyers fear the “95% LTV Premium.” It is true that 5% deposit mortgages carry higher rates than 40% deposit deals. However, in April 2026, lenders like Santander and Atom Bank have been cutting rates on high-LTV products.

Current 95% LTV rates are hovering around 5.2% to 5.5%. While this is higher than the 1% or 2% rates seen years ago, it must be compared against rental inflation. While your mortgage payment stays fixed (if you choose a fixed-rate deal), your rent is likely to increase by 2-3% every year.

4. Upfront Costs: It’s More Than Just the Deposit

The biggest hurdle for the 5% route is the upfront cash. For an average UK property of £268,000, a 5% deposit is £13,400. But you must also budget for:

- Stamp Duty: In 2026, first-time buyers pay £0 SDLT on properties up to £300,000.

- Conveyancing & Fees: Budget between £1,500 and £2,500 for legal work and searches.

- Surveys: A RICS Level 2 survey (essential in 2026) costs roughly £400-£900.

At Mortgage Bazaar, we help you calculate the Total Cost of Acquisition so there are no nasty surprises on completion day.

4. The “Freedom to Buy” Advantage

In 2026, the Mortgage Guarantee Scheme (Freedom to Buy) is a permanent fixture. This government-backed scheme gives lenders the confidence to offer 95% mortgages to buyers who have strong incomes but smaller savings.

If you are a Skilled Worker Visa holder or Self-Employed, Mortgage Bazaar can help you access these schemes where high-street banks might hesitate.

5. The “Risk” Factor: Negative Equity

The main argument against a 5% deposit is the risk of negative equity—where your home’s value drops below the mortgage balance.

- The 2026 Reality: UK house prices are currently growing at a stable 1.3% annually. This slow, steady growth is actually the “safest” environment for low-deposit buyers, as it significantly reduces the chance of a market crash.

The Verdict: Should You Buy or Rent?

| Category | Renting in 2026 | Buying with 5% Deposit |

| Monthly Cost | Higher (and rising annually) | Lower (fixed for 2-5 years) |

| Asset Growth | Zero | Building equity every month |

| Control | Limited (Landlord can sell) | Full (You are the owner) |

| Upfront Cost | Low (1 month deposit) | Moderate (£15k – £20k total) |

Conclusion: If you have the savings for a 5% deposit and plan to stay in the property for at least 3 to 5 years, buying is the clear financial winner. You stop paying someone else’s mortgage and start investing in your own future.

How Mortgage Bazaar Can Help

Navigating 95% LTV mortgages requires a specialist touch. We don’t just look for the lowest rate; we look for the lender with the most favorable criteria for your specific situation.

- Expert Comparison: We compare 200+ lenders to find the best 95% deals.

- Agreement in Principle (AIP): Get yours in under 24 hours to start bidding on homes.

- Fast Completion: Our 14-day average processing time gets you out of your rental and into your home faster.

Ready to escape the rent trap?

Speak to a Mortgage Bazaar advisor today for a free, no-obligation cost-benefit analysis of your specific situation.

- WhatsApp us: +44 7760747504

- Email: nikhil@mortgagebazaar.co.uk

- Visit us: www.mortgagebazaar.co.uk

Disclaimer: THINK CAREFULLY BEFORE SECURING OTHER DEBTS AGAINST YOUR PROPERTY | YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Visit us: - https://g.page/r/CfbGE7O83tmREAE

- https://www.facebook.com/mortgagebazaaruk

- https://www.instagram.com/mortgagebazaaruk

- https://www.linkedin.com/company/mortgagebazaar

Leave a Reply