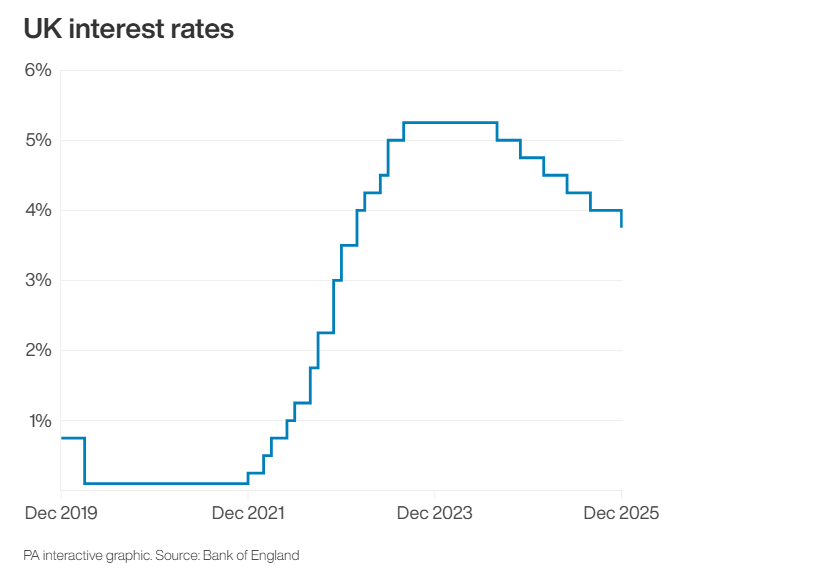

The Bank of England’s decision to cut the base interest rate to 3.75% marks a notable turning point for the UK housing and mortgage market. After an extended period of elevated borrowing costs, the move reflects growing confidence that inflationary pressures are easing and that the economy is entering a more balanced phase.

While this is not a return to the ultra-low interest rate environment of previous years, it signals a clear shift toward a more supportive backdrop for borrowers — particularly first-time buyers.

Inflation Outlook: Why This Cut Matters

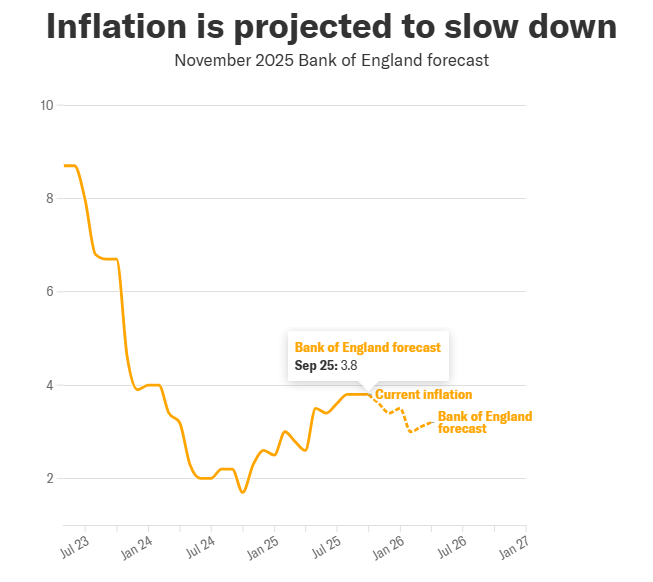

Minutes from the Monetary Policy Committee (MPC) meeting provide important context behind the decision. While inflation remains above the Bank’s 2% target, policymakers now expect headline inflation to fall back more quickly than previously forecast, potentially reaching close to target levels as early as April.

This represents a meaningful change from the Bank’s November projection, which had suggested inflation would not return to target until early 2027.

The MPC also highlighted that measures announced in the Autumn Budget, delivered by Chancellor Rachel Reeves, are expected to reduce CPI inflation by around 0.5 percentage points. These developments have reinforced confidence that underlying inflation pressures are easing faster than anticipated.

Bank of England Governor Andrew Bailey noted that while interest rates are on a “gradual path downward,” each cut will be assessed carefully:

“With every cut we make, how much further we go becomes a closer call.”

A Cooling Economy Shapes Policy

The rate cut also reflects a slowing economic backdrop. Recent data showed the UK economy contracted by 0.1% in October, and the MPC expects no growth in the final quarter of 2025. A weakening jobs market, slower pay growth, and easing energy costs are all contributing to reduced inflationary pressure.

CPI inflation fell to a four-month low of 3.6% in October, driven by slower rises in gas and electricity prices compared to last year. Economists widely expect this cooling trend to encourage further policy easing if conditions allow.

Chancellor Rachel Reeves commented:

“Under this government, we have seen five interest rate cuts that have helped bring down costs for families and businesses, and today’s forecast shows that inflation is due to fall faster than previously predicted.

What’s Happening in the Mortgage Market

Mortgage rates are influenced not only by the base rate, but also by swap rates, lender funding costs, and market expectations. In recent weeks, many lenders had already begun adjusting pricing in anticipation of this cut — particularly on fixed-rate products.

As a result, the market is now seeing:

- Increased lender competition, especially for first-time buyers

- Gradual improvements in fixed and tracker mortgage pricing

- More flexible affordability assessments as stress-testing eases

This creates a more constructive environment for buyers who may have struggled to qualify over the past 18–24 months.

Why This Matters for First-Time Buyers

First-time buyers are typically the most sensitive to interest rate movements due to higher loan-to-value borrowing and tighter affordability margins. Even modest reductions in rates can:

- Lower monthly repayments

- Improve borrowing capacity

- Increase confidence when making long-term commitments

However, timing and product choice remain critical. Not all lenders pass on rate cuts at the same pace, and fixing into the wrong mortgage structure too early can limit flexibility if rates continue to fall.

Mortgage Bazaar: Strategic Advice in a Changing Market

Commenting on the decision, Mortgage Bazaar said:

“The Bank of England’s decision to cut rates to 3.75% marks an important inflection point for the housing market. For first-time buyers in particular, this move improves confidence, lender appetite, and long-term affordability. However, not all mortgage products respond equally, and timing remains critical.

Our role is to ensure clients don’t simply react to headlines, but make informed, strategic decisions that protect them over the life of their mortgage- says Nikhil Bhatia CEO of Mortgage Bazaar Limited.”

At Mortgage Bazaar, advice is grounded in market insight and long-term planning.

The team:

- Monitors lender behaviour and pricing trends in real time

- Identifies lenders actively responding to market changes

- Structures mortgages that balance today’s opportunity with tomorrow’s resilience

The Bigger Picture

A base rate of 3.75% does not transform the market overnight, but it clearly represents momentum in the right direction. Falling inflation, a cooling economy, and a more competitive mortgage market are aligning to create genuine opportunity — particularly for prepared first-time buyers.

With the right guidance, this period can be one of confidence rather than caution.

Speak to Mortgage Bazaar

📞 Call 07760747504

🌐 www.mortgagebazaar.co.uk

✉️ nikhil@mortgagebazaar.co.uk

There is no charge for initial consultation. Get your FREE mortgage eligibility assessment done today.

Mortgage Bazaar supports first-time buyers with expert insight, whole-of-market access, and mortgage strategies designed to stand the test of time.

The Bigger Picture

A base rate of 3.75% does not transform the market overnight, but it does represent momentum in the right direction. For prepared buyers with the right guidance, this period offers genuine opportunity.

Mortgage Bazaar supports first-time buyers with expert insight, whole-of-market access, and mortgage strategies designed to stand the test of time.

#mortgagebazaar #mortgageadvisor #mortgagerate #interestrates